Most people who file an insurance claim expect the insurer to pay. Those whose claims are rejected feel betrayed , they paid premiums for years, they needed the cover, and the payout was denied. Understanding why claims are rejected, and what policyholder behaviour prevents rejection, is as important as any coverage decision you make.

The Six Most Common Reasons for Claim Rejection

- Non-disclosure of pre-existing conditions

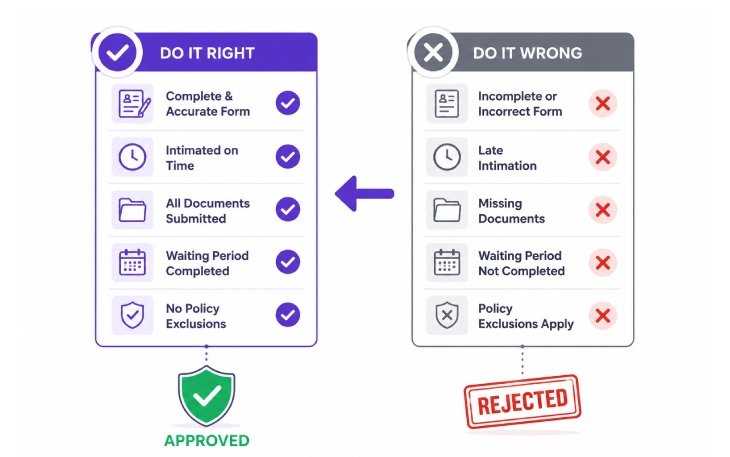

The most common reason, and the most avoidable. Insurance contracts operate on the principle of utmost good faith , you must disclose all material facts about your health and risk profile at the time of purchase. A known pre-existing condition that was not disclosed gives the insurer legal grounds to void the entire policy and reject any claim not just claims related to the undisclosed condition. Always disclose truthfully. The waiting period is far less damaging than a rejected claim.

- Policy exclusions

The treatment is specifically excluded from the policy. Cosmetic procedures, fertility treatments, conditions within waiting periods, treatments beyond sub-limits , these rejections are technically correct. The remedy is understanding exclusions before buying, not challenging them after claiming.

- Late intimation

Most policies require intimation within 24–48 hours of a hospitalisation. For planned admissions, 48–72 hours before. Missing this window is a commonly cited reason for rejection. IRDAI’s regulations now require insurers to demonstrate actual prejudice from delayed intimation rather than rejecting purely on procedural grounds but the safest approach is always to notify the insurer immediately.

- Treatment during the waiting period

Filing a claim for a condition that falls within the policy’s waiting period will be rejected. This applies even if the policyholder was unaware of the condition at the time of purchase if the insurer can demonstrate the condition existed before the waiting period expired, the claim is outside policy scope.

- Documentation deficiencies

A valid claim can be delayed or rejected for incomplete documentation. For health claims: original bills, discharge summary, prescription, diagnostic reports, and claim form. For motor claims: FIR copy where required, repair bills, RC book, driving licence. Submit documents in the format specified by the insurer.

- Misrepresentation in the claim form

Incorrect dates, inconsistent information, or inflated amounts in the claim form trigger scrutiny and can result in rejection even where the underlying event is genuine. Complete every field accurately.

What to Do If Your Claim Is Rejected

A rejection must be provided in writing with the stated reason. Assess whether the rejection is justified. If not, escalate through the insurer’s grievance process. If unresolved within 30 days, file a complaint at igms.irda.gov.in. The Insurance Ombudsman handles disputes up to ₹30 lakh, is free of charge, and its decisions are binding on the insurer.

Draco Insurance supports clients through every claim from documentation to dispute resolution at no extra cost. Visit dracoinsurance.in or call +91 7064106417.

“Even if we do not talk about 5G (specifically), the security talent in general in the country is very sparse at the moment. We need to get more (security) professionals in the system”

Bharti Airtel, for example, has been preparing for 5G roll out by upskilling its professionals and offering them certification courses such as CCNA (Cisco Certified Network Associate) and CCNP (Cisco Certified Network Professional). The courses are offered based on skill and eligibility level free of cost.