If you have been diagnosed with diabetes, hypertension, thyroid disorders, or any other chronic condition before buying health insurance, one clause matters above all others: the pre-existing disease waiting period. Not understanding it is one of the most common reasons claims get rejected not due to fraud, but because the policyholder simply was not aware.

What Counts as a Pre-Existing Disease

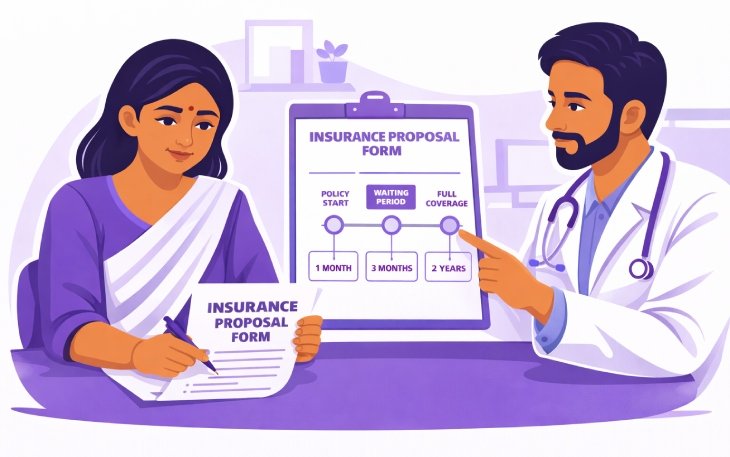

As per IRDAI’s (Insurance Products) Regulations 2024 effective , a pre-existing disease is any condition diagnosed or treated by a physician within 36 months before the date your policy commences. The lookback period was reduced from 48 months to 36 months under these updated regulations. If you had a condition within this 36-month window, it counts as PED , regardless of whether you disclosed it or not.

How the Waiting Period Works

As of April 1, 2024, IRDAI has capped the maximum PED waiting period at 36 months (3 years). Previously policies could impose up to 48 months. During this waiting period, if you are hospitalised for something directly linked to your pre-existing condition, the insurer can deny the claim. After the waiting period ends, the condition is covered exactly like any other illness.

Many insurers offer reduced waiting periods of 1 to 2 years. A handful of plans offer PED coverage from Day 1 if a medical examination is cleared at the time of purchase. Also from April 2024, the moratorium period after which an insurer cannot investigate any claim on grounds of non-disclosure was reduced from 8 years to 5 years.

Disclosure Is Non-Negotiable

Hiding a condition to avoid a higher premium or a longer waiting period is the costliest mistake you can make in insurance. If discovered at claim time, which insurers routinely investigate the claim will be rejected and the policy may be cancelled entirely. Complete honesty at purchase is what protects you.

The Portability Credit

If you have served part of a waiting period with your current insurer, that credit transfers when you switch insurers through portability. You do not restart the clock. This is a significant benefit when you find a better plan at renewal , the time you have already served with one insurer is not lost.

What Is Covered From Day One

Accidents, emergencies unrelated to your pre-existing condition, and many other medical events are covered immediately from Day 1. Read your policy document carefully to know which conditions have waiting periods and which are covered from the start.

Confused about waiting periods or whether your health history affects coverage options? Draco Insurance’s advisors can walk you through the fine print. Visit dracoinsurance.in or call +91 7064106417.

“Even if we do not talk about 5G (specifically), the security talent in general in the country is very sparse at the moment. We need to get more (security) professionals in the system”

Bharti Airtel, for example, has been preparing for 5G roll out by upskilling its professionals and offering them certification courses such as CCNA (Cisco Certified Network Associate) and CCNP (Cisco Certified Network Professional). The courses are offered based on skill and eligibility level free of cost.