- Medical inflation in India is running at approximately 14% annually (ACKO Health Insurance Index 2024). Cost-sharing structures chosen now have compounding financial implications over a 20-year policy tenure.

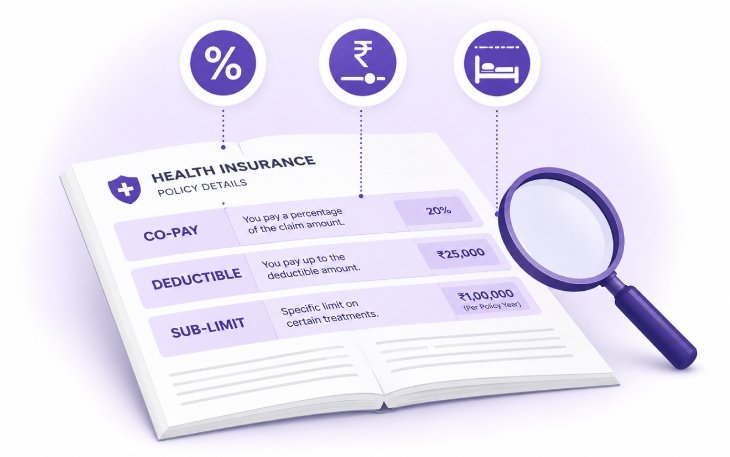

A sub-limit caps how much the insurer pays for a specific component of a claim. The most consequential: room rent sub-limits. A policy capping room rent at 1% of sum insured per day allows a ₹5,000/day room on a ₹5 lakh policy. If you stay in an ₹8,000/day room, you pay the ₹3,000 difference but the impact extends further.

Most policies with room rent caps apply proportionate deduction: doctor fees, surgery, diagnostics, and all associated costs are also reduced proportionately based on the room upgrade percentage. A 60% room cost excess can reduce total claim payout by 35–50%. This is the most common cause of claim shock in Indian health insurance.

| Clause | Better Option | Watch For |

| Co-pay | Zero co-pay or voluntary only | Mandatory co-pay in senior citizen plans |

| Deductible | Aggregate (optional) if you have corporate cover | Per-claim deductible instead of aggregate |

| Room rent sub-limit | No limit or single private room without cap | 1% of SI cap triggering proportionate deduction |

| Illness sub-limit | No disease-specific caps | Fixed limits for cataract, hernia, knee replacement |

Draco Insurance compares policy fine print not just premiums across 15+ insurers to find plans that protect you at claim time. Visit dracoinsurance.in or call +91 7064106417.

“Even if we do not talk about 5G (specifically), the security talent in general in the country is very sparse at the moment. We need to get more (security) professionals in the system”

Bharti Airtel, for example, has been preparing for 5G roll out by upskilling its professionals and offering them certification courses such as CCNA (Cisco Certified Network Associate) and CCNP (Cisco Certified Network Professional). The courses are offered based on skill and eligibility level free of cost.