Choosing health insurance for parents above 60 is one of the most consequential financial decisions in a family’s insurance planning. Medical needs are higher, premiums are steeper, and the fine print matters significantly more than at any other life stage. Several regulatory changes since 2024 have improved options for senior citizens in India but navigating them requires understanding what changed and what to look for.

What IRDAI’s 2024 Regulations Changed for Senior Citizens

Under IRDAI’s Insurance Products Regulations 2024 (effective April 1, 2024):

- No insurer can refuse to sell a health policy solely on grounds of age. The previous maximum entry age of 65 that many insurers imposed has been removed

- Maximum waiting period for pre-existing diseases capped at 36 months down from 48 months previously

- Moratorium period reduced from 8 years to 5 years: after 5 continuous years of coverage, no insurer can reject claims on grounds of non-disclosure of pre-existing conditions (unless fraud is proven)

- Insurers are required to offer dedicated senior citizen health insurance products with features tailored for older age groups

- IRDAI capped annual premium increases for senior citizens at 10% per year , protecting against sudden, steep renewal hikes

IRDAI circular (January 30, 2025): insurers cannot increase senior citizen health insurance premiums by more than 10% annually at renewal.

The Five Key Things to Check When Buying for Parents Above 60

- Pre-existing condition waiting period

Parents above 60 almost always have at least one pre-existing condition — hypertension, diabetes, thyroid, joint issues. The waiting period for these conditions determines when claims related to them become eligible. Under IRDAI rules, the maximum is now 36 months, but many plans offer shorter periods. Prioritise plans with the shortest PED waiting period for your parents’ specific conditions.

- Co-pay clause

Many senior citizen health plans include a mandatory co-pay of 10–20%. A 20% co-pay on a ₹15 lakh surgery means your parents pay ₹3 lakh themselves. Look for plans with zero co-pay or a voluntary co-pay option. If co-pay is unavoidable, understand the exact percentage and calculate its impact on likely claim scenarios.

- Room rent sub-limits

Senior citizen plans are more likely to include room rent sub-limits than standard plans. As established in Blog 1 of this set, a room rent cap triggers proportionate deduction on the entire claim bill. Look for plans with no room rent sub-limit, or at minimum a single private room entitlement without a percentage cap.

- Restoration benefit

A restoration benefit reinstates the sum insured after it is partially or fully exhausted in a year. For senior citizens with multiple health issues who may make more than one hospitalisation claim in a year, a restoration benefit ensures the sum insured is available for subsequent claims in the same year.

- Network hospitals near your parents’ home

A high sum insured policy is only practical if your parents can access cashless treatment at hospitals they can actually reach. Check that the insurer’s cashless network includes quality hospitals in your parents’ city and area, not just aggregate hospital count nationally.

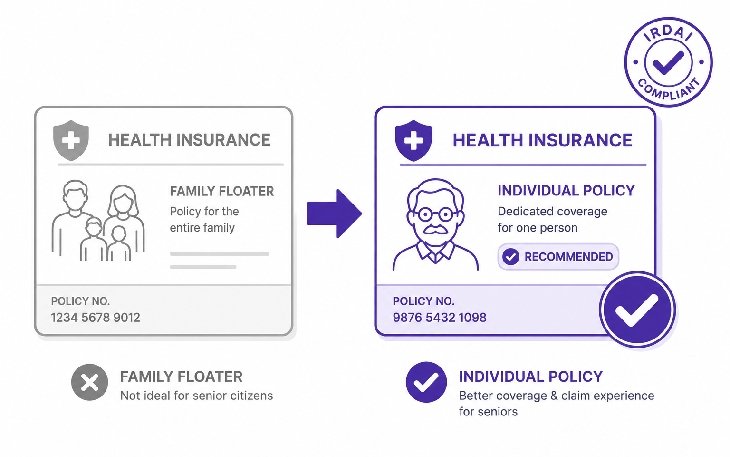

Buying as Part of a Family Floater vs Individual Policy

Including parents above 60 in a family floater plan significantly increases the premium for the entire family because the insurer prices the pooled risk upward. In most cases, buying a separate individual policy for parents is more cost-effective than adding them to a family floater. The exception: when parents are below 60, are in good health, and the floater sum insured is sufficient for all members.

Section 80D Tax Benefit for Parents’ Insurance

Premiums paid for health insurance for parents above 60 qualify for a deduction of up to ₹50,000 per year under Section 80D under the old tax regime. This is in addition to the ₹25,000 deduction for your own and your family’s health insurance. If both you (below 60) and your senior citizen parents are covered, total 80D deduction can be up to ₹75,000 per year.

Draco Insurance compares senior citizen health plans across 15+ insurers evaluating co-pay, PED waiting periods, room rent terms, and hospital network to find the right cover for your parents. Visit dracoinsurance.in or call +91 7064106417.

“Even if we do not talk about 5G (specifically), the security talent in general in the country is very sparse at the moment. We need to get more (security) professionals in the system”

Bharti Airtel, for example, has been preparing for 5G roll out by upskilling its professionals and offering them certification courses such as CCNA (Cisco Certified Network Associate) and CCNP (Cisco Certified Network Professional). The courses are offered based on skill and eligibility level free of cost.