Health insurance top-up and super top-up plans are among the most cost-effective ways to increase your health coverage in India yet most people have never heard of them. If you currently have a ₹5 lakh corporate cover or a basic individual policy, a top-up plan can extend your protection to ₹25 or ₹50 lakhs at a fraction of the cost of buying a full plan at that sum insured.

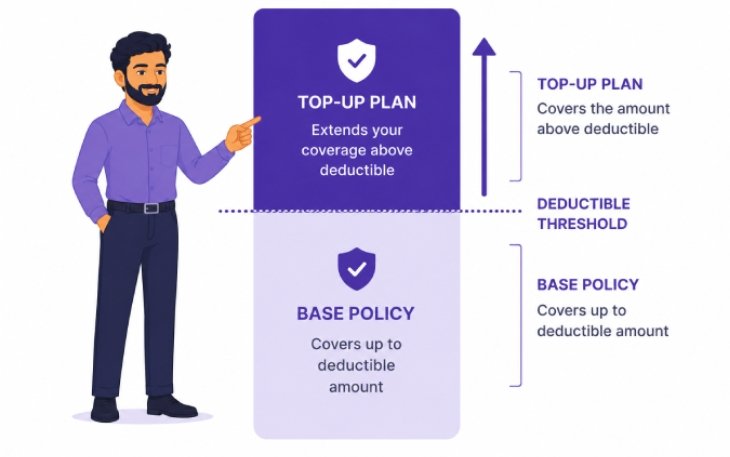

What a Top-Up Plan Is

A top-up health insurance plan activates when a single claim crosses a pre-defined threshold called the deductible. The insurer pays nothing below the deductible. Above it, the top-up plan covers the excess up to its sum insured.

Example: You have a ₹5 lakh base policy and buy a ₹20 lakh top-up with a ₹5 lakh deductible. If a hospitalisation bill is ₹12 lakh, your base policy pays ₹5 lakh and the top-up pays ₹7 lakh. Total out of pocket: zero (assuming the base policy fully covers its limit).

A ₹50 lakh top-up plan with a ₹5 lakh deductible for a 35-year-old in a metro city costs approximately ₹6,000–10,000 per year in 2026 — a fraction of what a standalone ₹50 lakh policy would cost.

The Critical Limitation: Per-Claim Deductible

A top-up plan’s deductible applies separately to each individual claim. If you have three hospitalisations in a year totalling ₹12 lakh each costing ₹4 lakh none individually crosses the ₹5 lakh deductible, so the top-up plan pays zero. The base policy handles each claim separately.

What a Super Top-Up Plan Is and Why It Solves This

A super top-up plan applies the deductible to the aggregate of all claims in a policy year, not each claim individually. With the same scenario , three claims of ₹4 lakh each, total ₹12 lakh – a super top-up with a ₹5 lakh annual aggregate deductible pays ₹7 lakh (₹12L minus ₹5L deductible).

| Feature | Top-Up Plan | Super Top-Up Plan |

| Deductible applies per | Individual claim | Aggregate of all claims in the year |

| Best for | Catastrophic single claims | Multiple smaller claims in a year |

| Premium | Slightly lower | Slightly higher than top-up |

| Recommended for most buyers | For young, healthy individuals | For families or those with chronic conditions |

Who Should Buy a Top-Up or Super Top-Up Plan

- Employees with corporate health cover of ₹3–5 lakh who want catastrophic protection without replacing the employer policy

- Individuals with a basic ₹5 lakh policy who cannot afford a higher base premium but want significantly more cover

- People in their 30s and 40s who want to lock in high coverage at low premium before medical conditions develop

- Families where the annual sum insured across all members could realistically be exhausted by one major illness

Tax Benefit

Premiums paid for top-up and super top-up health plans qualify for deductions under Section 80D of the Income Tax Act under the old tax regime, in addition to premiums paid for the base policy. This makes them doubly efficient for taxpayers in higher brackets who have already used the base 80D limit.

Draco Insurance helps you identify the right top-up structure and deductible level to complement your existing health cover. Visit dracoinsurance.in or call +91 7064106417.

“Even if we do not talk about 5G (specifically), the security talent in general in the country is very sparse at the moment. We need to get more (security) professionals in the system”

Bharti Airtel, for example, has been preparing for 5G roll out by upskilling its professionals and offering them certification courses such as CCNA (Cisco Certified Network Associate) and CCNP (Cisco Certified Network Professional). The courses are offered based on skill and eligibility level free of cost.