Most people sign their health insurance policy without reading the document. That’s understandable — they can be long and written in legal language. But a few specific sections determine whether your claim gets paid. Here’s where to focus.

The Inclusions List — and the Sub-Limits Within It

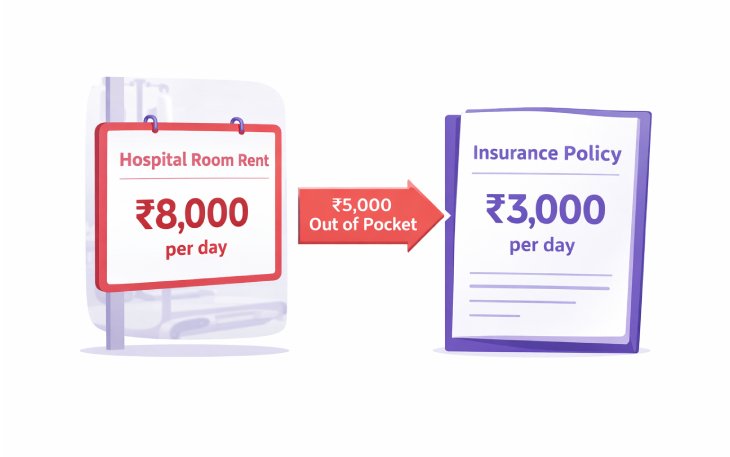

The inclusions list tells you what’s covered. But look carefully for sub-limits — caps on specific expenses like room rent per day, ICU charges, or particular procedures. A policy covering room rent at ₹3,000 per day in a hospital that charges ₹8,000 means you pay the ₹5,000 difference yourself, every day, even though you have insurance. These sub-limits can significantly reduce the actual benefit of a policy.

The Exclusions List: Read This First

The exclusions list tells you what your policy will not cover under any circumstances. Common permanent exclusions across most policies include: cosmetic or aesthetic treatments, self-inflicted injuries, war or nuclear events, and experimental treatments. Check whether dental and vision care are excluded, as they often are. Knowing your exclusions before you need to claim is essential.

Waiting Periods Section

Waiting periods specify how long you must have the policy before certain conditions are covered. There’s typically an initial waiting period of 30 days for any claim (except accidents). Pre-existing disease waiting periods are now capped at 3 years by IRDAI. Specific disease waiting periods — for named conditions like joint replacement or cataracts — can be up to 2 years. The moratorium period is 5 years, after which most non-disclosure related rejections are not possible.

The Claim Procedure Section

This section tells you exactly what steps to follow and what documents to submit when you need to make a claim. For cashless claims, you need to inform the insurer’s TPA (third-party administrator) before or within a specific time of hospitalisation.

For reimbursement claims, all original bills and medical reports must be submitted within a specified period after discharge. Missing these steps is one of the most avoidable reasons claims face delays or rejection.

Renewal Terms and Lifetime Renewability

Check that your policy guarantees lifetime renewability. Some older policies had upper renewal age limits — if your insurer decides not to renew after you reach a certain age, you lose coverage precisely when you need it most. Under IRDAI’s current guidelines, insurers must offer at least one product with no upper age limit, but your specific policy terms still govern your particular plan.

Draco Insurance helps you understand your policy document and what to do when you need to make a claim. Call +91 7064106417 or visit dracoinsurance.in

“Even if we do not talk about 5G (specifically), the security talent in general in the country is very sparse at the moment. We need to get more (security) professionals in the system”

Bharti Airtel, for example, has been preparing for 5G roll out by upskilling its professionals and offering them certification courses such as CCNA (Cisco Certified Network Associate) and CCNP (Cisco Certified Network Professional). The courses are offered based on skill and eligibility level free of cost.